Taking Stock: A Longview Into Markets, Credit, and the Year Ahead

Every so often it’s worth taking a breath, stepping back, and asking a simple question:

Because if you look at the headlines alone, you’d think we’re sitting on the edge of catastrophe. But if you look at the data — properly look at it — the story is far more nuanced.

Over the last couple of months I’ve been watching several themes develop across markets, credit, earnings, valuations, and global activity. As we head into the final stretch of the year, here’s where I think we actually stand.

1. Gold: Genius or Fool’s Playground?

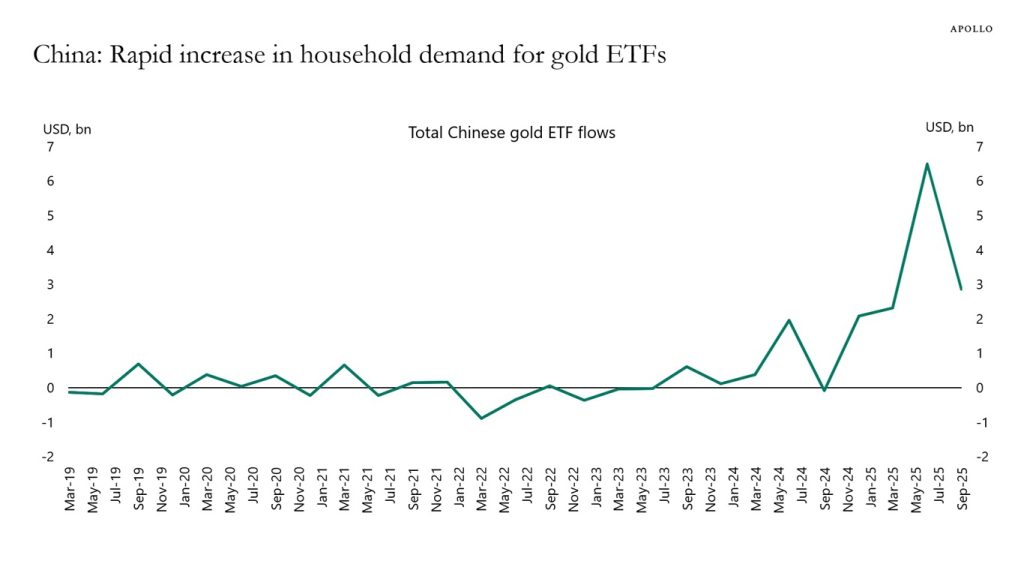

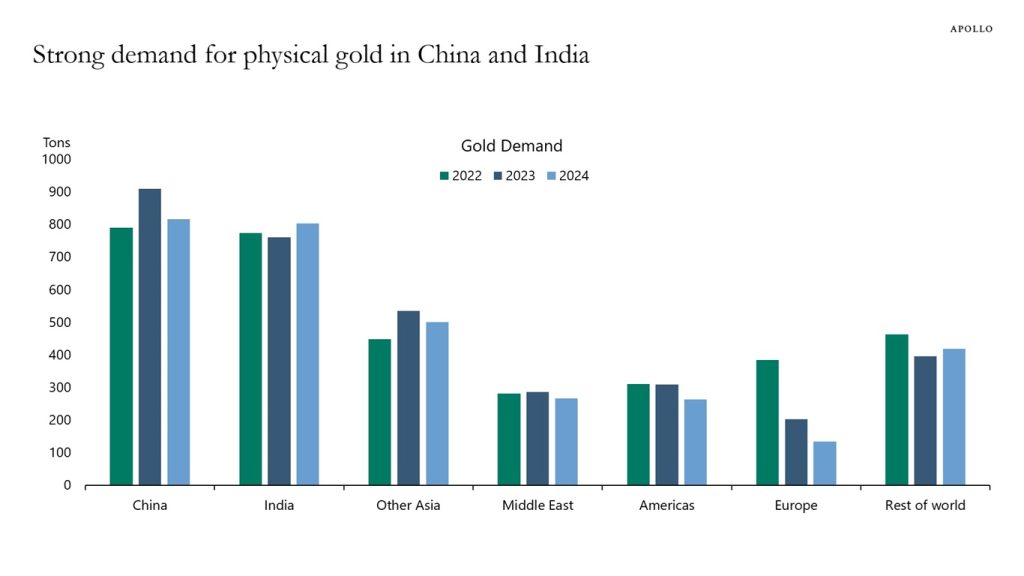

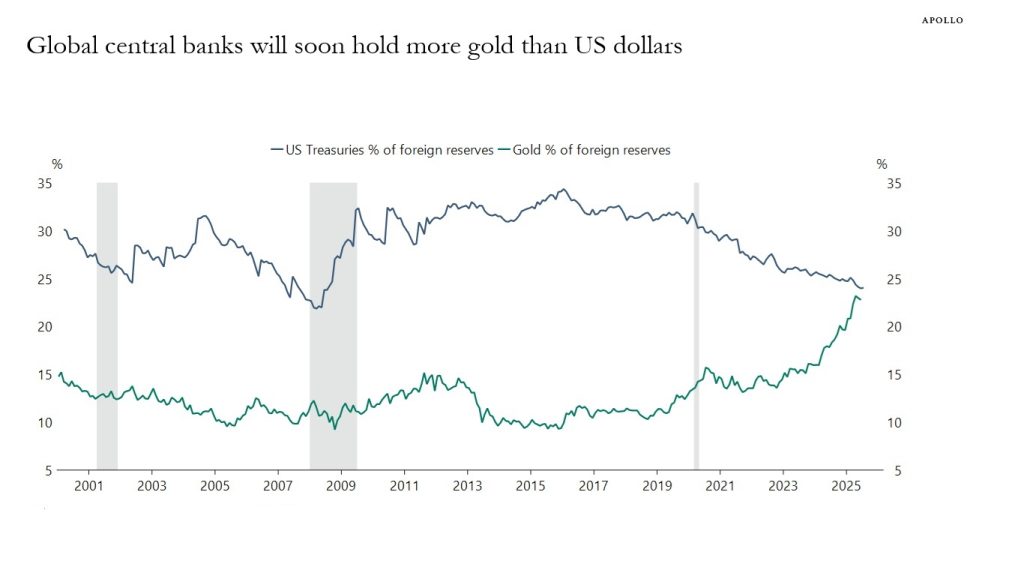

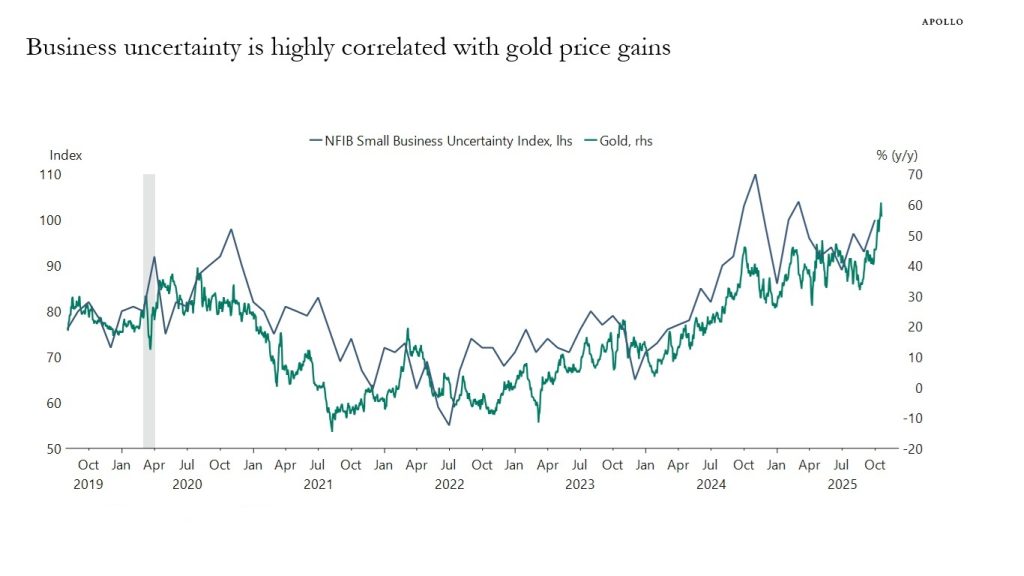

Gold has become the trade du jour. People lining up in Sydney to buy coins without the faintest idea why. China buying aggressively. Global central banks shifting reserves from dollars into hard metal. Retail speculation exploding. Business uncertainty rising in the US — historically a strong driver of gold prices.

It all makes for a compelling story.

But to me, right now, the move in gold feels stretched. Prices have run hard, sentiment is euphoric, and the narrative is doing a lot of heavy lifting. I’m not calling it a mania — there’s still a lot of water to go under the bridge before we can say that. But when something rallies this far, this fast, without a clear shift in fundamentals, I prefer to stay cautious rather than chase. I’m not a buyer at these levels.

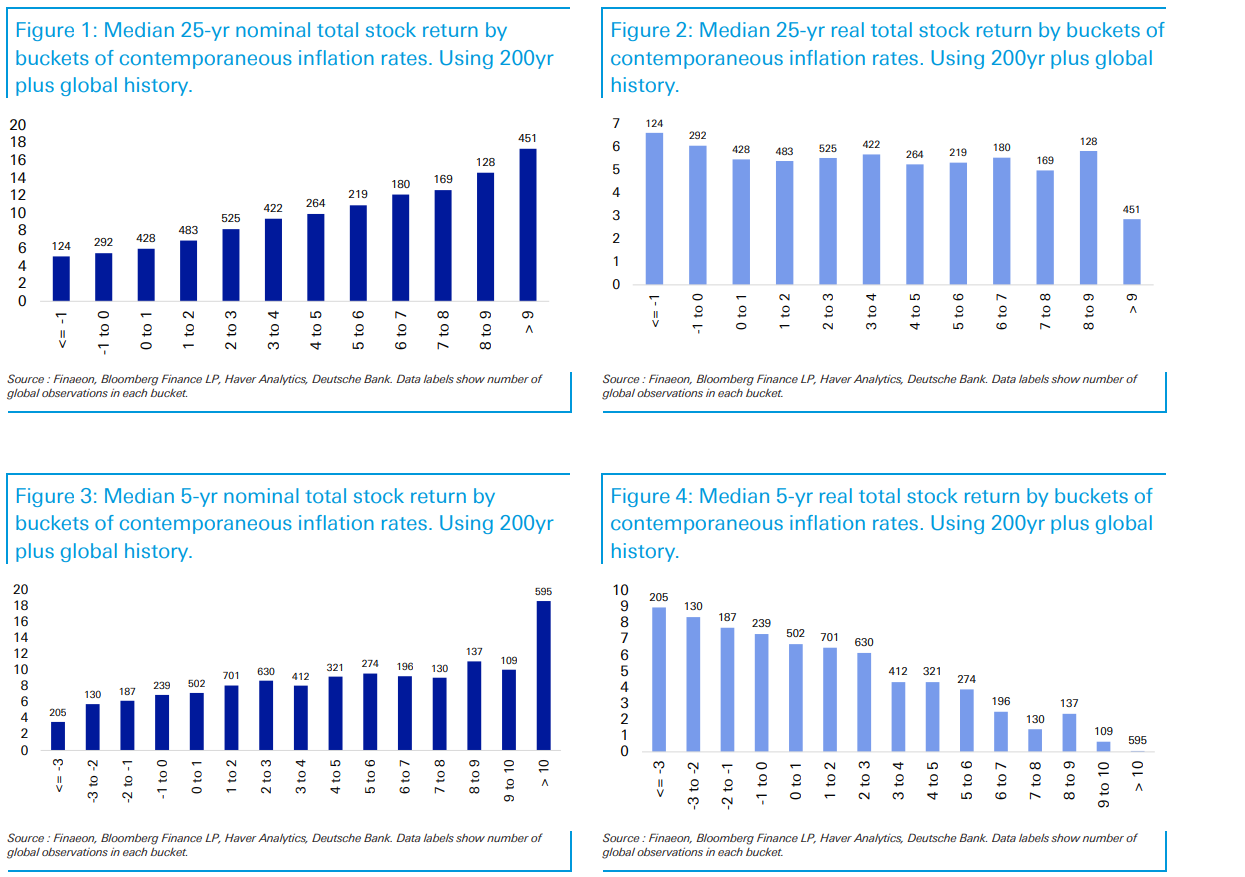

2. Inflation: Equities Still Win (Most of the Time)

One of the most common questions I hear is:

“How do equities behave in different inflation regimes?”

The most comprehensive dataset ever assembled — 200+ years, 56 countries, thousands of rolling periods — gives us a clear answer:

- Over 25 years: equities are exceptional inflation hedges in nominal terms.

- In real terms: high inflation does hurt, but the real damage only occurs at extreme inflation levels.

- Over 5 years: real returns fall almost linearly as inflation rises.

So if you believe we’re entering a structurally higher inflation environment, equities still give you a fighting chance. Just expect a bumpier ride.

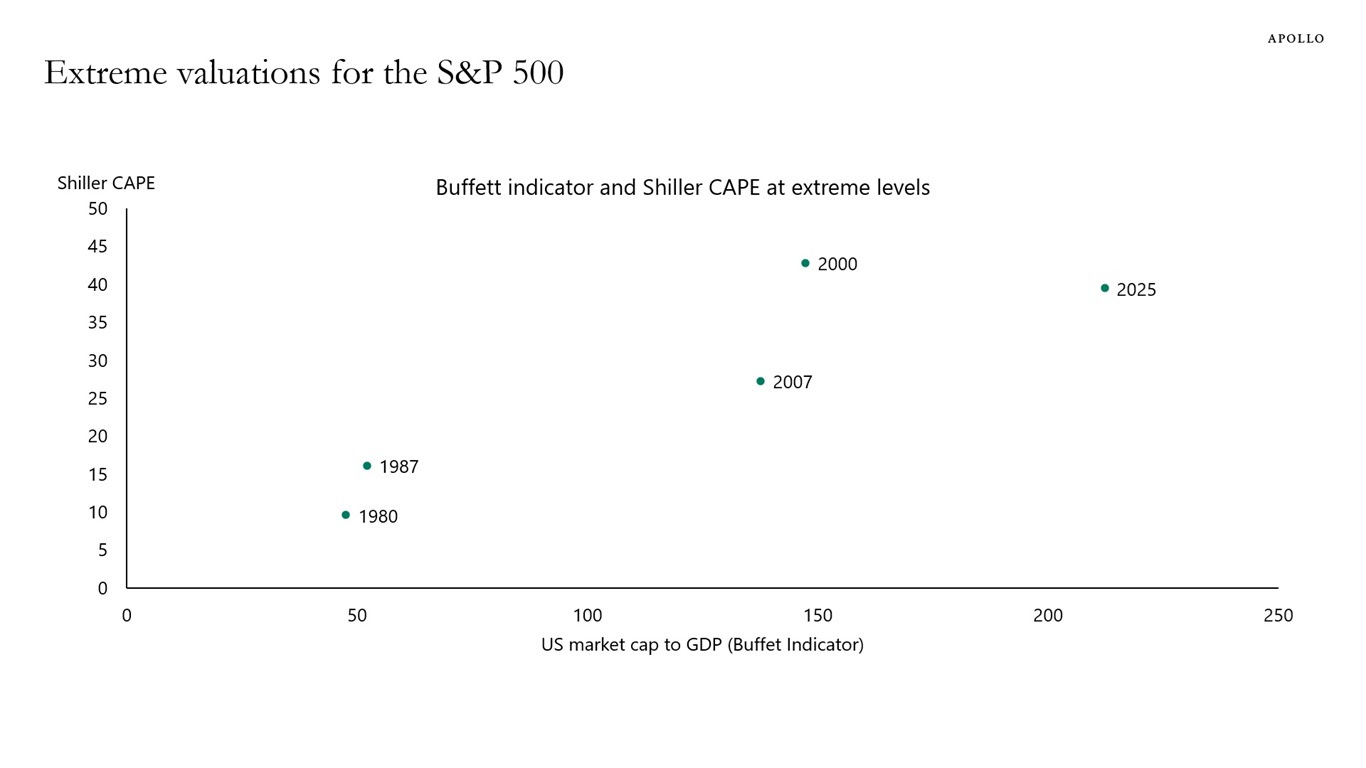

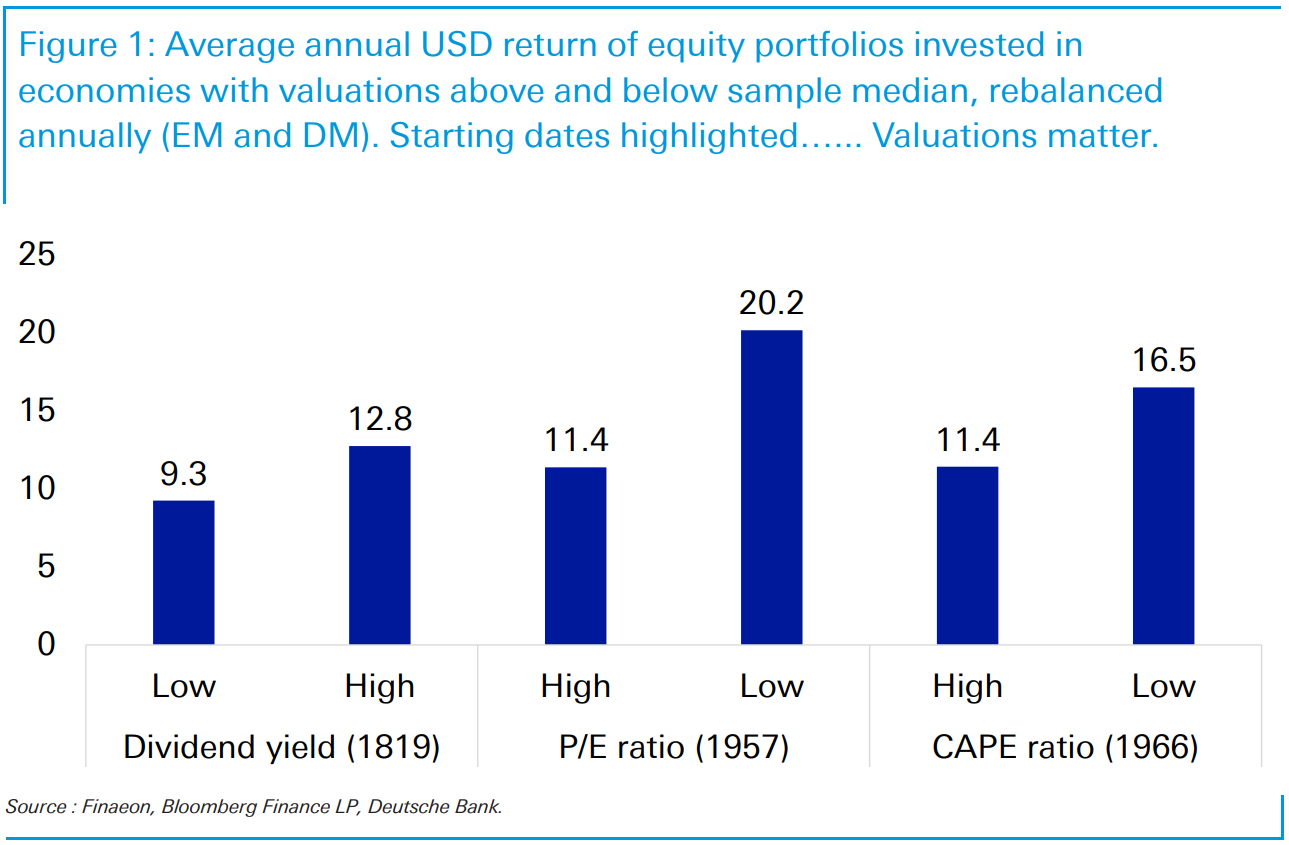

3. Valuations: Expensive for a Reason?

Let’s be honest — US equity valuations are high. Buffett indicator. CAPE. Forward P/E. Take your pick.

They all scream “expensive.”

But expensive assets can keep getting more expensive when earnings continue to rise. And earnings, not opinions, are what drive markets over time.

Every valuation dataset from the Long-Term Study leads to one consistent conclusion:

Starting valuations matter — massively.

Cheap markets outperform expensive ones over and over again.

Today, the US sits firmly in the “expensive” bucket. But that doesn’t automatically make it uninvestable. It just reduces your margin for error.

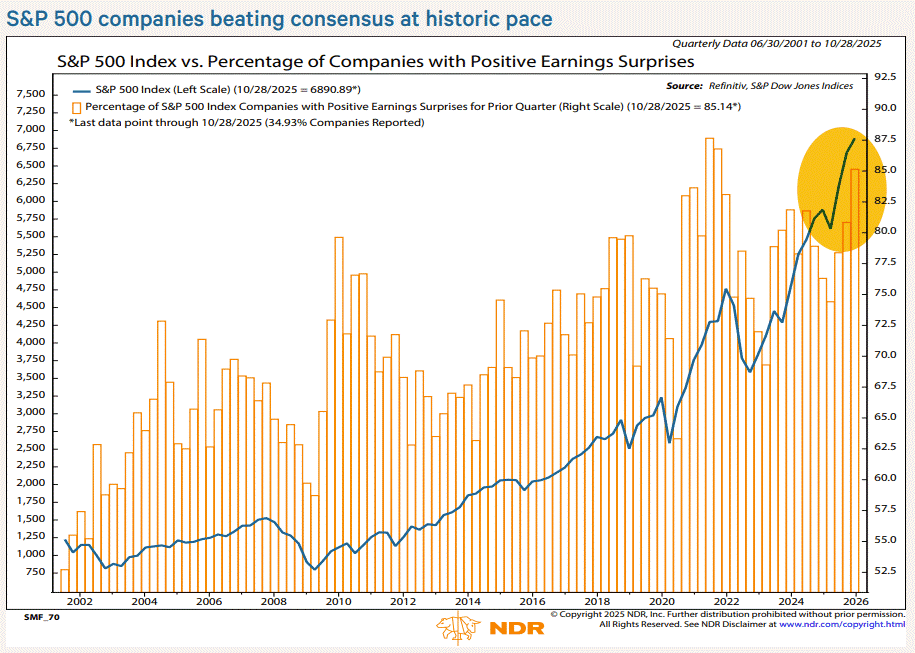

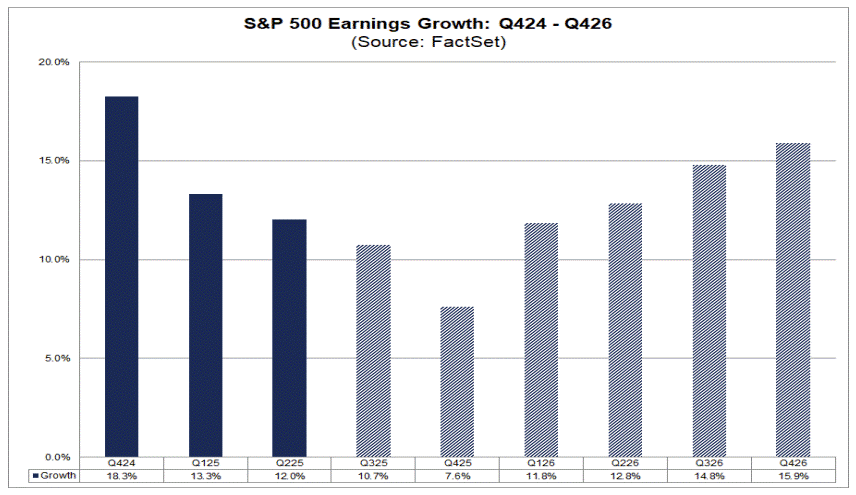

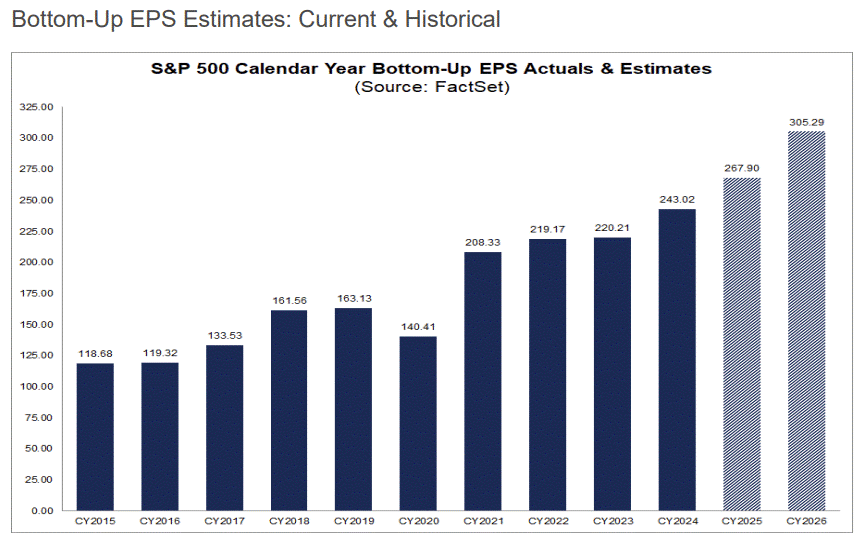

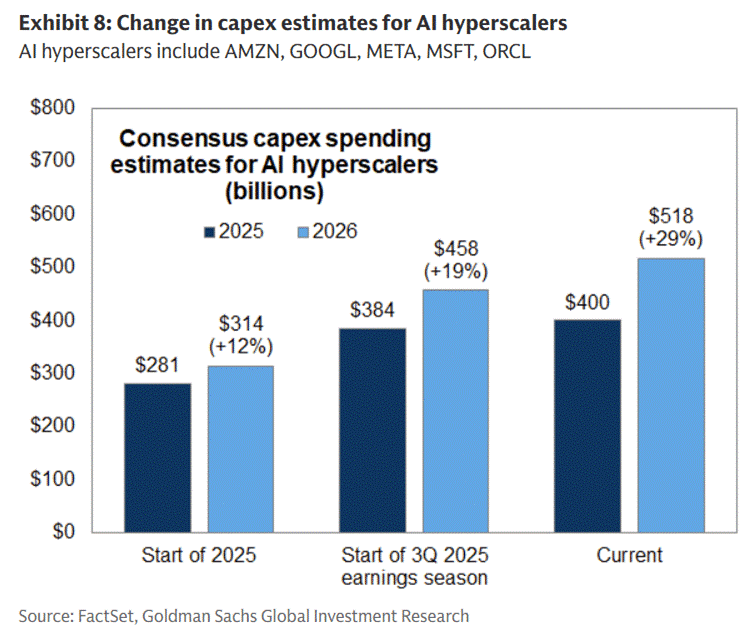

4. Earnings: The Heartbeat of the Rally

This earnings season has been one of the strongest in recent history.

- 84% of companies beating expectations

- Double-digit EPS growth

- Earnings surprising at a historic pace

- Forecasts showing strong growth into 2026

- AI hyperscalers ramping CapEx aggressively

- The Magnificent Seven producing $1 million of profit every minute

Say what you want about market enthusiasm, but corporate America is delivering. And that matters far more than any short-term noise.

The rally hasn’t been driven by profits alone — multiple expansion has played a role — but the earnings foundation is solid.

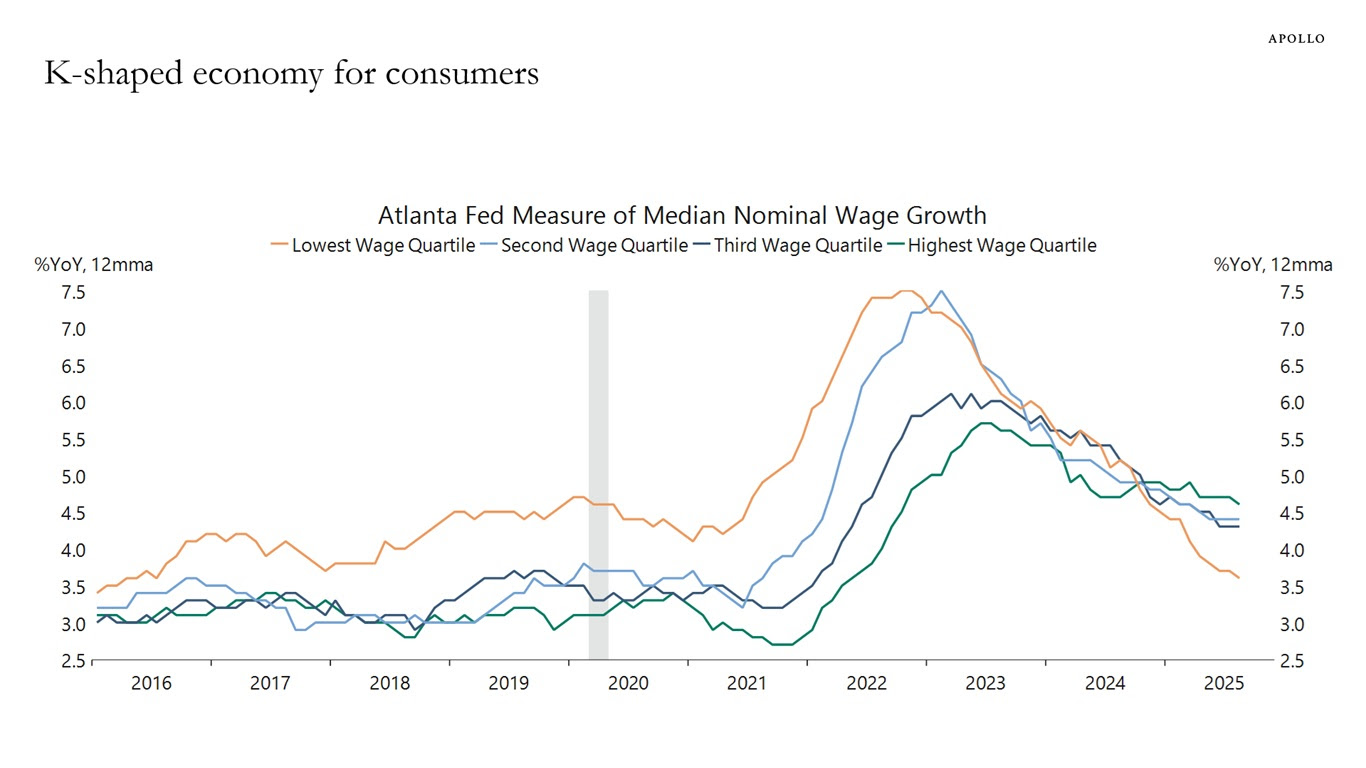

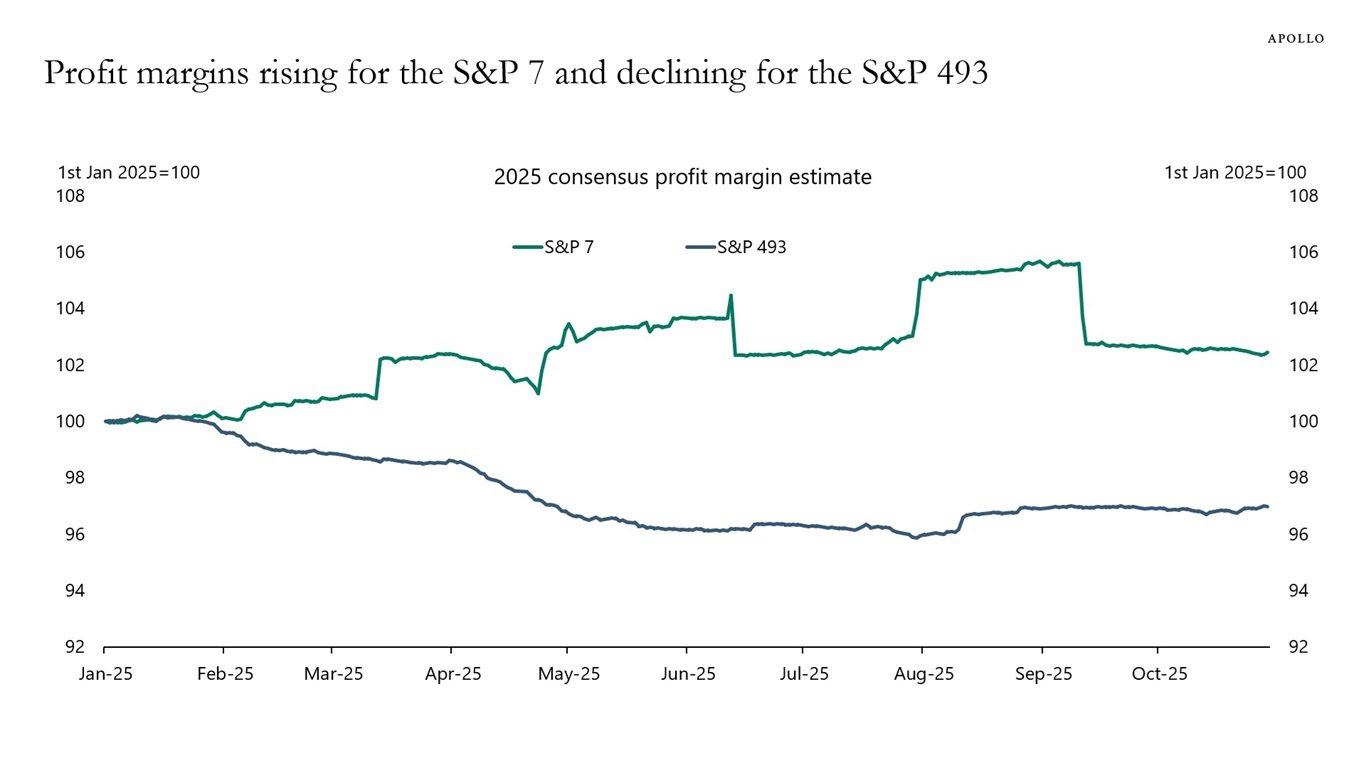

5. The K-Shaped Economy: Households and Corporates Split

Beneath the surface, not everyone is thriving.

For consumers:

- Lower-income wage growth has rolled over

- Higher-income groups are pulling away again

- The pandemic’s temporary equalisation has reversed

For corporates:

- The “Magnificent 7” are expanding margins

- The “S&P 493” are seeing margins decline

- Earnings expectations are being revised up for the Mag 7 and down for everyone else

This is a K-shaped world: a small group accelerating while the majority grinds.

And markets are reflecting this reality.

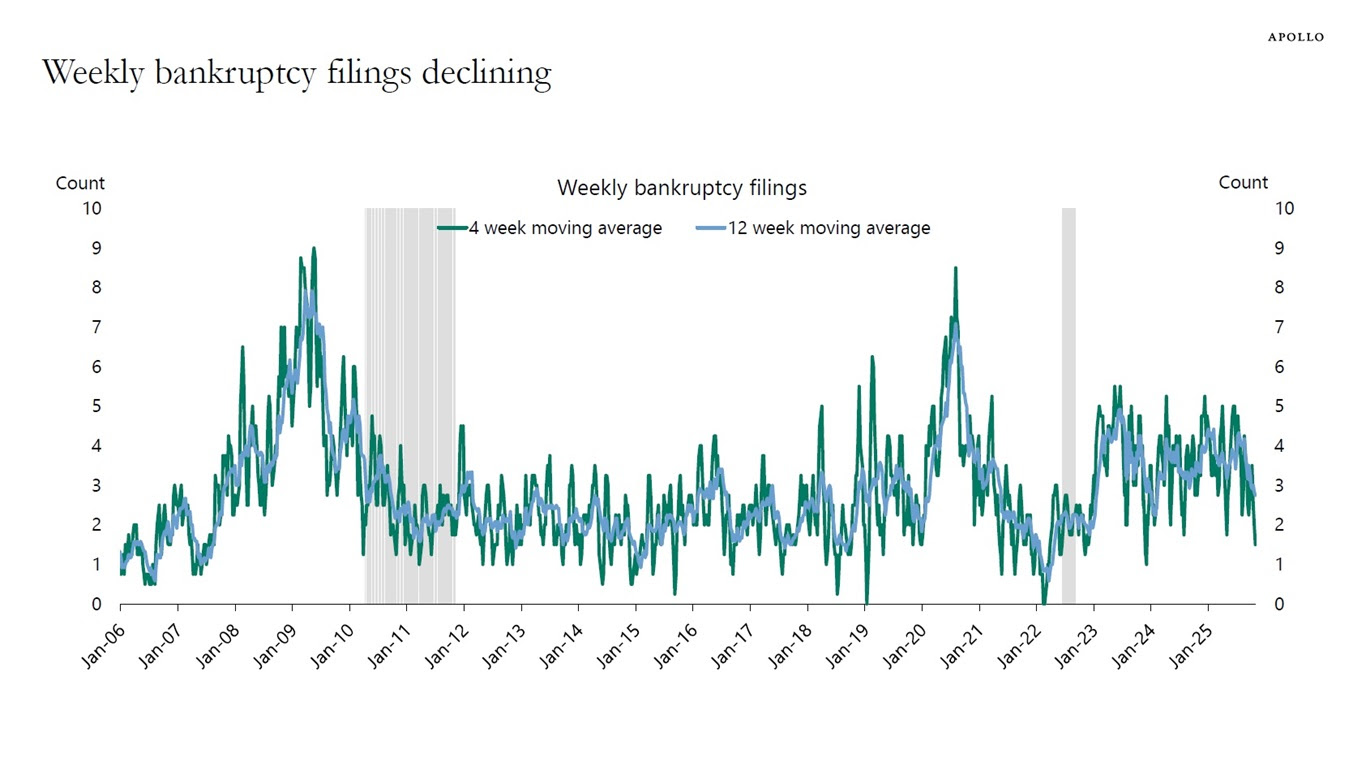

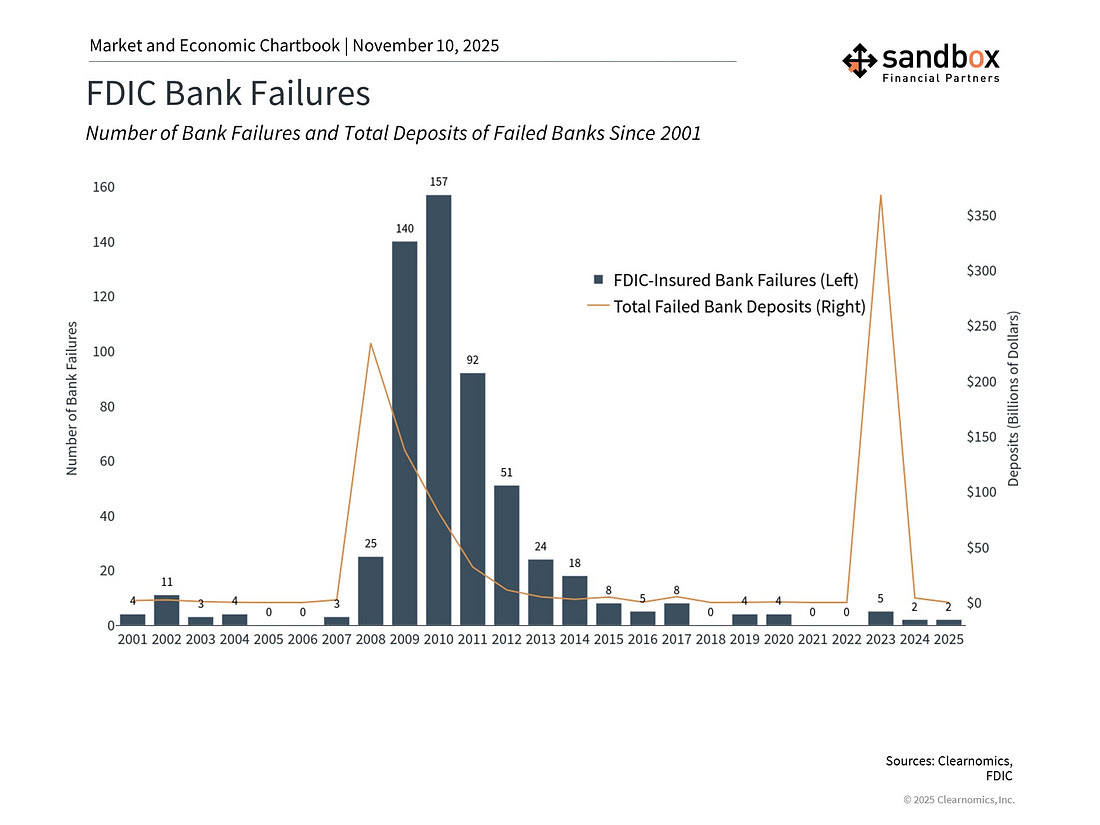

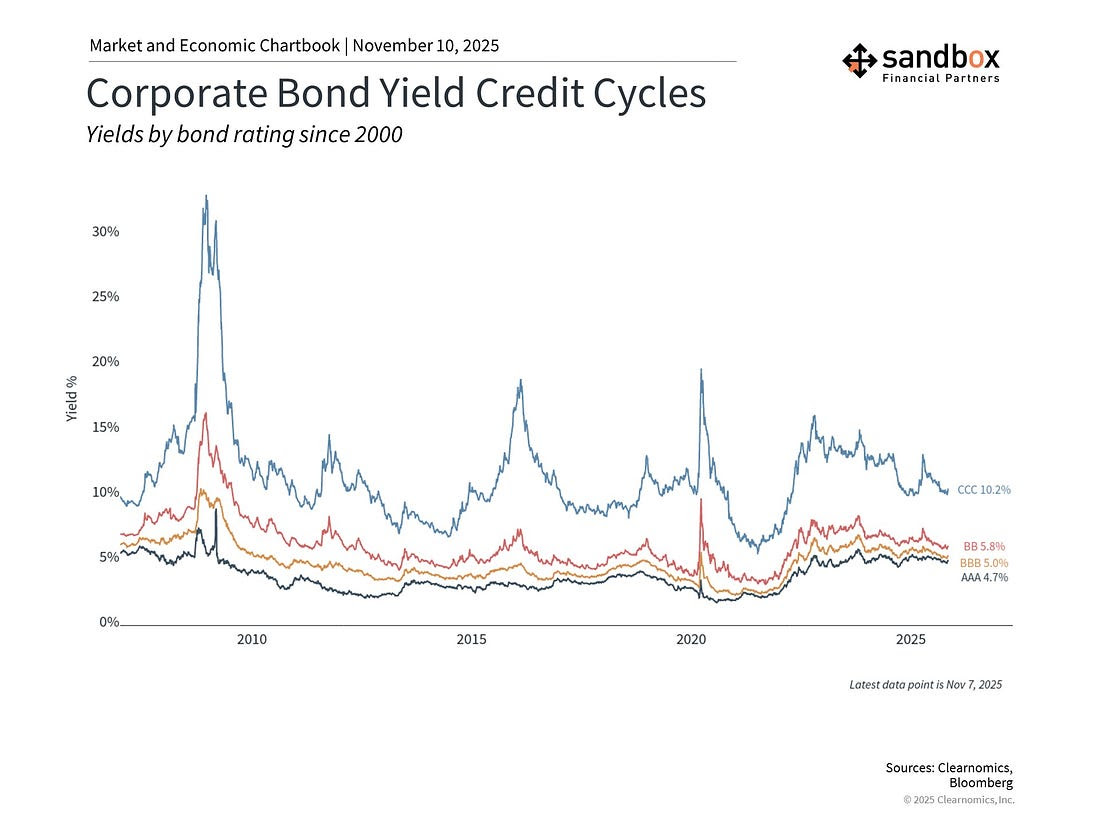

6. Credit: Cracks, Cockroaches, and Context

A few borrowers have fallen over in recent months and — as Jamie Dimon put it — “when you see one cockroach…”

Fair point. But we need perspective.

This isn’t 2008.

This isn’t 2023.

This isn’t a system that’s leveraged to the eyeballs.

Bankruptcies have been falling.

Bank failures are minimal.

Bond market volatility has normalised. Corporate yields aren’t flashing systemic stress.

Yes, private credit has grown rapidly. Yes, frauds happen. Yes, underwriting discipline varies widely. But right now, the credit cycle looks more like a systems check, not the start of contagion.

And this is why manager selection matters more in private credit than almost any other asset class — dispersion of returns is enormous.

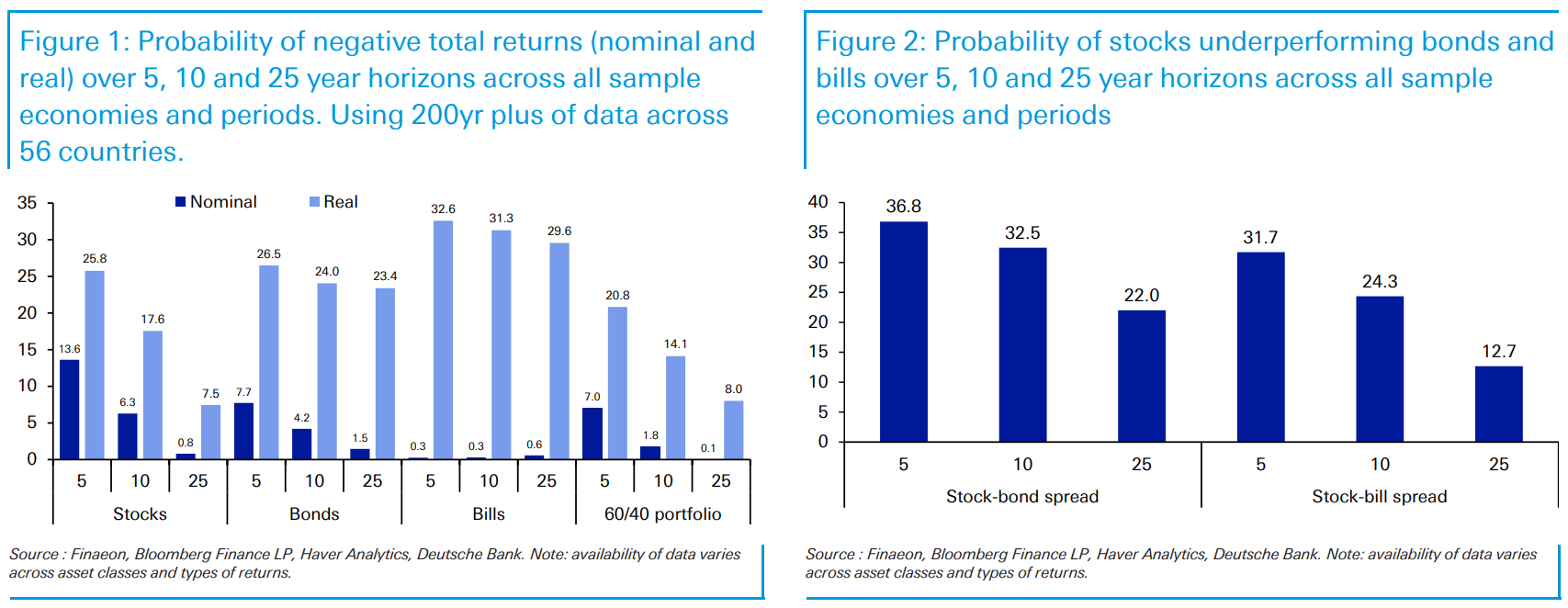

7. Probability of Loss: What History Actually Says

Over 200 years of global data:

- 5-year nominal equity losses: ~14% of periods

- 25-year nominal equity losses: <1%

- 25-year real equity losses: ~7%

- Bonds: far more vulnerable, especially in real terms

- 60/40 portfolios: almost zero probability of nominal loss over 25 years

In other words:

Time is a hedge. Diversification is a hedge. Valuations are a hedge. Cash is not.

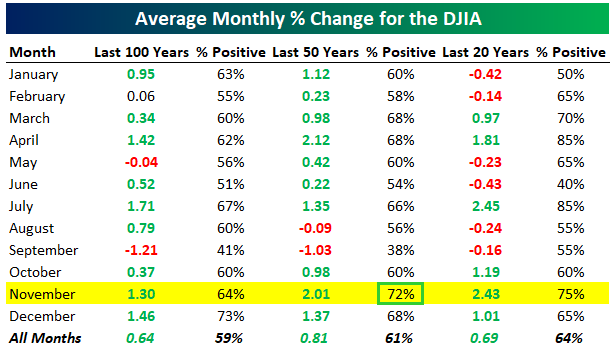

8. Seasonality & Market Structure: History on Our Side

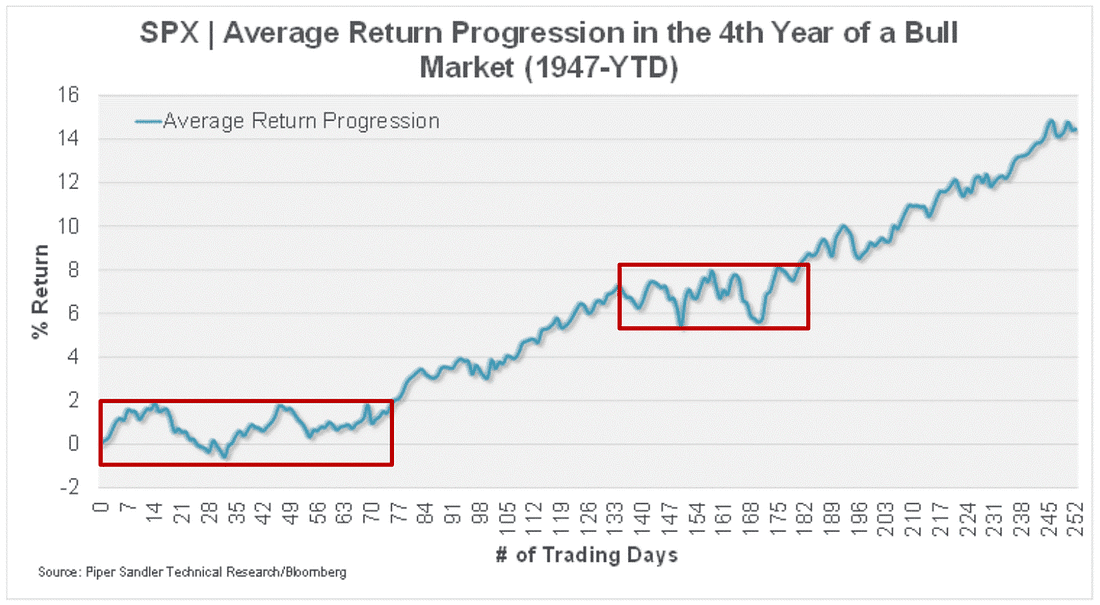

We’ve now entered year four of the bull market that began in October 2022.

Since World War II:

- 6 of the last 7 bull markets that reached year four kept rising

- Median one-year return: +12.9%

- We’re only 775 days into a bull market whose median lifespan is 979 days

Year fours typically start with a consolidation phase — which we’ve seen — then push higher.

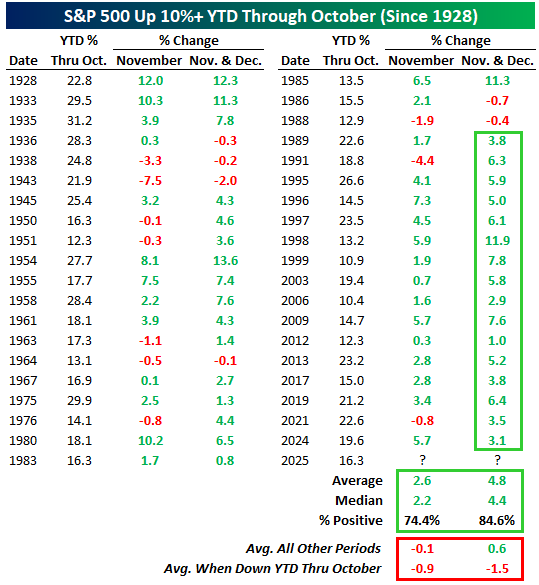

Seasonality is also a quiet tailwind:

- “Santa Claus Rally” historically starts around now

- November and December are two of the strongest months on record

- When the S&P is up 10%+ YTD through October (like this year), Nov–Dec returns are significantly stronger

History doesn’t guarantee anything, but it stacks probabilities in your favour.

9. Five Tailwinds Heading Into Year-End

1. A Pickup in Global Activity

Growth momentum globally is turning up, not down.

2. Tax Cuts

A fiscal tailwind for both consumers and corporates.

3. Tariff Uncertainty Fading

A significant reduction in the chaos premium markets were pricing.

4. Interest Rate Cuts

We’re entering an easing cycle into rising markets — a rare but powerful combination.

5. Momentum

And finally, the one tailwind people love to dismiss: momentum. Strong markets tend to stay strong. Gains beget gains.

10. Final Thoughts: Getting the Big Things Right

Markets today are noisy, contradictory, and emotional. But when you zoom out, the major themes become more obvious:

- Gold is running hot — too hot.

- Inflation remains sticky but manageable.

- Valuations are high, yet earnings are strong.

- Credit cracks exist, but systemic risks are limited.

- The Mag 7 continue to dominate — for real fundamental reasons.

- Seasonality and history are quietly supportive.

- Tailwinds outweigh headwinds as we head into year-end.

We don’t invest in headlines. We don’t invest in fear. We invest in fundamentals, probabilities, and time. And right now, the weight of evidence suggests this market still has room to run — not without risk, not without setbacks, but with enough structural support to keep moving higher.

Ready to grow your wealth?

Let's talk. One call. No risk. Just a way to see if we're a good fit.